Global cloud services market Q1 2021

Shanghai (China), Bengaluru (India), Singapore, Reading (UK) and Portland (US) – Thursday, 29 April 2020

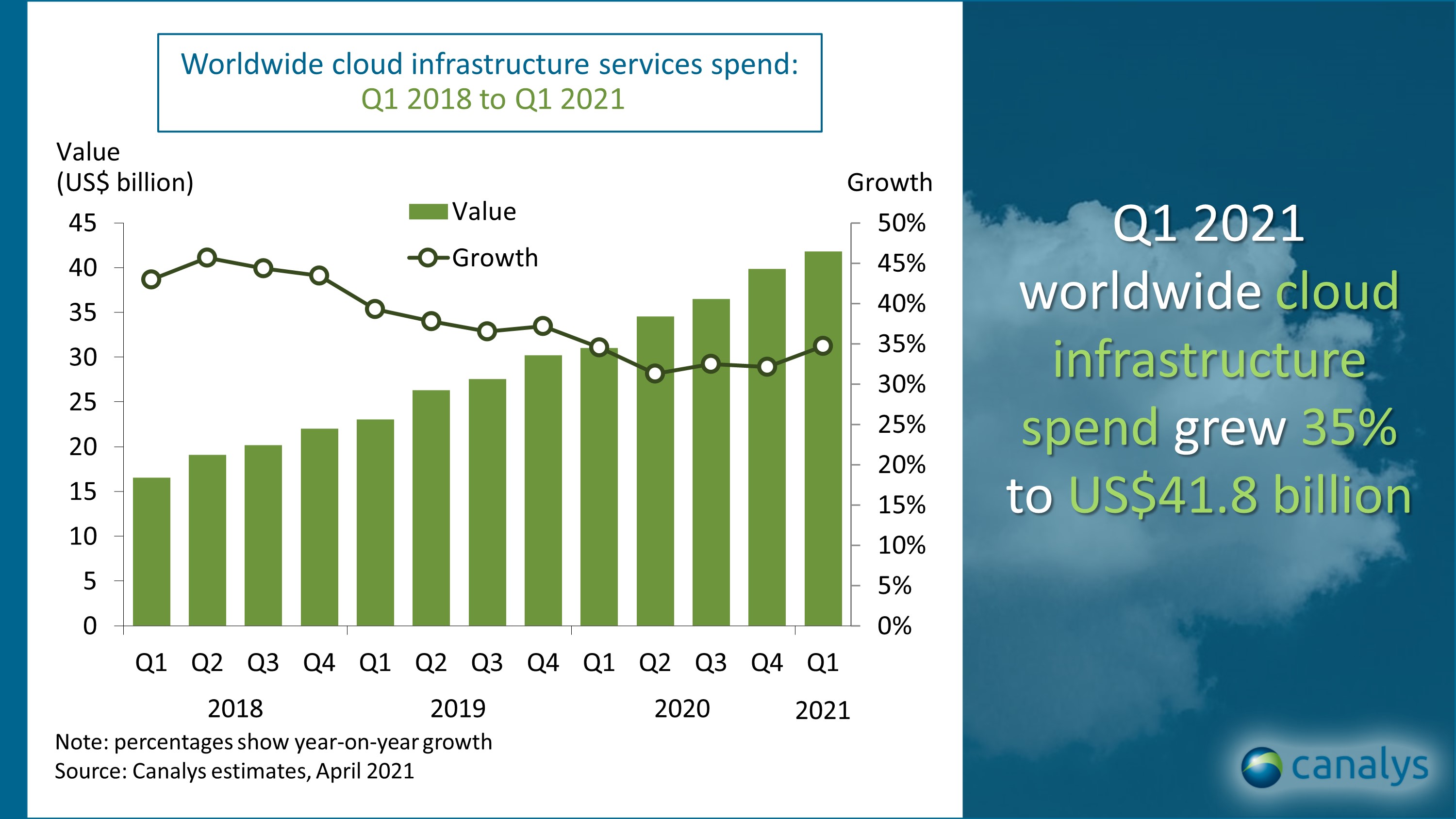

Canalys: Global cloud services market reaches US$42 billion in Q1 2021

Cloud infrastructure services spending grew 35% to US$41.8 billion in the first quarter of 2021. The trend of using cloud services for data analytics and machine learning, data center consolidation, application migration, cloud native development and service delivery continued at pace. Overall, customer spending exceeded US$40 billion a quarter for the first time in Q1, with total expenditure nearly US$11 billion higher than in Q1 2020 and nearly US$2 billion more than in Q4 2020, according to Canalys data. The acceleration of digital transformation over the last 12 months, with organizations adapting to new working practices, customer engagement, and business process and supply chain dynamics, has elevated demand for these services. This, combined with the rebound in some economies, in line with government stimuli, the roll-out of mass COVID-19 vaccination programs and subsequent easing of restrictions, has increased customer confidence in committing to multi-year contracts.

Amazon Web Services (AWS) was the leading cloud service provider in Q1 2021, growing 32% on an annual basis to account for 32% of total spend. In the last quarter it announced new CloudFront edge locations in Croatia and Indonesia and extended its Wavelength Zones for 5G networks to Japan and across the United States. It launched its new EX2 X2gd instances based on the AWS-designed Graviton2 CPU for memory-intensive workloads and improved price-performance.

Microsoft Azure grew 50% for the third consecutive quarter, taking 19% market share in Q1 2021. Growth was boosted by cloud consumption and longer-term customer commitments enabled by investments in Azure Arc for hybrid-IT control plane management, Azure Synapse for data analytics, and AI as a platform. It introduced new industry clouds propositions for financial services, manufacturing and non-profit organizations, adding to healthcare and retail.

Google Cloud maintained its momentum, benefiting from its Google One approach driving cross-sell and integration opportunities across its portfolio. Overall, it grew 56% in the latest quarter to account for a 7% market share. Cloud-native development and accelerated cloud migration among its customers has been boosted by its focus on industry-specific solutions, machine learning, analytics and data management. It announced a new cloud region in Israel.

“Cloud emerged as a winner across all sectors over the last year, basically since the start of the COVID-19 pandemic and the implementation of lockdowns. Organizations depended on digital services and being online to maintain operations and adapt to the unfolding situation,” said Canalys Research Analyst Blake Murray. “Though 2020 saw large-scale cloud infrastructure spending, most enterprise workloads have not yet transitioned to the cloud. Migration and cloud spend will continue as customer confidence rises during 2021. Large projects that were postponed last year will resurface, while new use cases will expand the addressable market.” Investment at the edge, including 5G, is a key area, especially for the development of ultra-low latency applications and use cases, such as autonomous vehicles, industrial robotics and augmented or virtual reality.

Competition among the leading cloud service providers to capitalize on these opportunities will continue to intensify. “Geographic expansion for data sovereignty and to improve latency, either via full-region deployment or a local city point of presence, is one area of focus for the cloud service providers,” said Canalys Chief Analyst Matthew Ball. “But differentiation through custom hardware development for optimized compute instances, industry-specific clouds, hybrid-IT management, analytics, databases and AI-driven services is increasing. But it is not just a contest between the cloud service providers, but also a race with the on-premises infrastructure vendors, such as Dell Technologies, HPE and Lenovo, which have established competitive as-a-service offerings. The challenge will be demonstrating a differentiated value proposition for each.”

Canalys defines cloud infrastructure services as services that provide infrastructure as a service and platform as a service, either on dedicated hosted private infrastructure or shared infrastructure. This excludes software as a service expenditure directly, but includes revenue generated from the infrastructure services being consumed to host and operate them.

For more information, please contact:

Canalys China

Nicole Peng: nicole_peng@canalys.com +86 150 2186 8330

Canalys India

Rushabh Doshi: rushabh_doshi@canalys.com +91 99728 54174

Canalys Singapore

Sharon Hiu: sharon_hiu@canalys.com +65 9777 9015

Canalys UK

Matthew Ball: matthew_ball@canalys.com +44 7887 950 505

Alastair Edwards: alastair_edwards@canalys.com +44 7901 915 991

Canalys USA

Alex Smith: alex_smith@canalys.com +1 650 799 4483

Blake Murray: blake_murray@canalys.com +1 650 308 6687

About Canalys

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

Receiving updates

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please contact us. Alternatively, you can email press@canalys.com.

Please click here to unsubscribe

Copyright © Canalys. All rights reserved.

For more information:

e-mail press@canalys.com

PDF download

Global cloud services market Q1 2021

Global cloud services market Q1 2021