Southeast Asian smartphone shipments fall 7% sequentially in Q2 2022

Shanghai (China), Bengaluru (India), Singapore, Reading (UK) and Portland (US) – Monday, 15 August 2022

In Q2 2022, Southeast Asian smartphone shipments reached 24.5 million units, a 7% drop from the previous quarter. Consumer confidence has been severely hit by growing inflation and vendors are struggling to keep devices affordable in price-sensitive markets. The five largest markets in the region stalled this quarter as a result of the industry experiencing significant macroeconomic headwinds and the resulting strain on local consumer demand. Despite Ramadan season festivities for Malaysia and Indonesia, both countries saw smaller-than-expected sequential growth of 6% and 2% respectively. The Philippines market grew 4% versus the previous quarter due to increased spending during its elections. Thailand though was hit by severe forex depreciation against the USD and thus saw a 14% quarter-on-quarter decline. Meanwhile, Vietnam saw a 20% decline due to growing consumer uncertainty.

Key market dynamics

Indonesia

Indonesia remained the largest market in SEA, with 37% share and 9.1 million shipments driven by festive bonus payouts to Indonesians in celebration of Ramadan. Samsung led the market with 20% share and vivo's enhanced aggressiveness in both retail and online channels helped maintain its 19% market share cementing its second position. Transsion replaced realme at number five in Indonesia for the first time owing to its enhanced online branding push with Infinix. Infinix's Hot series attracted consumers in the sub-US$200 price range.

Philippines

The Philippines’ smartphone market remained the second largest market in SEA with 4.4 million shipments. It grew 4% against the previous quarter as vendor activity picked up in Q2. realme retook the top spot from Transsion, penetrating the mass-market segment via its volume-driver C35 series and increasing online channel activities using the Narzo series. Transsion, despite experiencing a sequential dip in Q2, was successful in meeting offline consumer demand in tier-2 cities and built distributor confidence. Meanwhile, Xiaomi and OPPO grew 10% and 55% quarter-on-quarter, respectively. Xiaomi’s growth was attributed to the popularity of its Redmi 10 series which was welcomed by offline channels.

Thailand

Thailand’s smartphone market declined 14% sequentially to 4.0 million units as the economy struggled due to a weakened Thai baht coupled with ballooning inflation and slow economic recovery. However, Xiaomi recovered against Q1, mainly driven by consumer demand for its volume-driver models across its offline channels. Smartphone vendors are looking to optimize channel efficiency in Thailand to reduce margin pressures. Thai operators have stepped up efforts in bundling and promotions to reignite consumer demand, although with varying degrees of effectiveness.

Vietnam

Vietnam’s smartphone market declined 32% quarter-on-quarter to 3.1 million shipments, as a result of weakened consumer demand stemming from global uncertainties and rising commodity prices. Vietnam remains a strategic country for Samsung as it leads the market with a 41% share. Samsung has managed to establish a strong partnership with the key distributor, ‘Mobileworld’ to maintain dominance in the Vietnam market, capturing most of Vinsmart’s exit market share. Despite a quarterly slowdown in smartphone shipment, Vietnam’s mid-high-end potential remains strong.

Malaysia

Malaysia’s smartphone market grew 6% to 2.4 million shipments versus Q1 2022, due to Hari Raya festivities and promotional activities which attempted to stimulate consumer demand. Samsung doubled its effort in the channel to push the shipment of its revamped A-series. Competition has reignited in low-end smartphones as ballooning inflation on commodities has led to a fall in mid-to-high-end smartphone demand. Vendors are stuck between a rock and a hard place, as they try to position themselves as economical brands in the high-demand entry-level segment while also dealing with rising operating costs.

Vendor performance

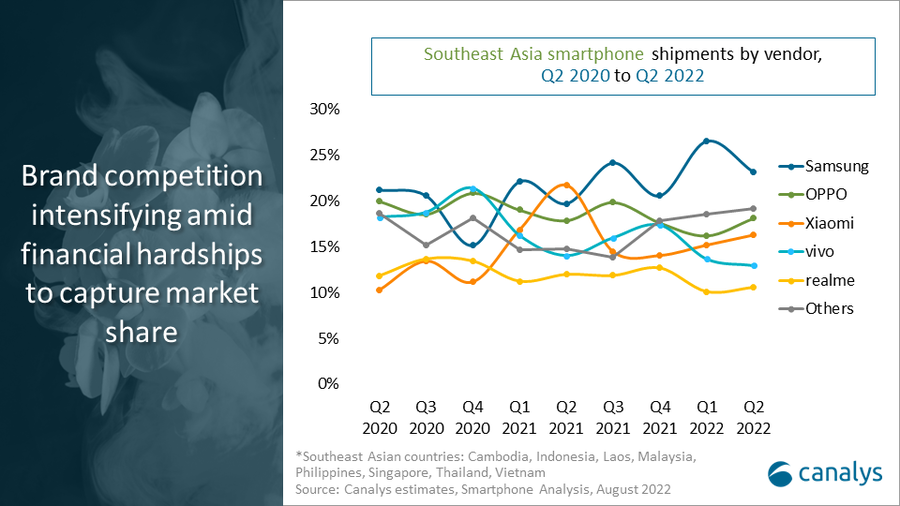

Samsung retained its leading position in Southeast Asia despite a 19% fall from Q1 2022 owing to lower than anticipated demand for its mid-to-high-end A series. The major marketing initiatives and channel incentives for Samsung's entry-level A-series have helped the company regain lost market share. Samsung’s extensive investment in above-the-line marketing campaigns on its foldables and S22 series sets it up to compete in the premium price segment.

OPPO maintained its strong performance in second spot with an 18% market share. This was attributed to robust demand for its A16 series which was SEA’s top-selling model. OPPO dropped the sub-US$100 price band in 2021 to drive its Reno series and strengthen its brand image with a degree of success. At the same time, OPPO is further increasing product-mix initiatives with the official launch of OnePlus Nord series into the region.

Xiaomi maintained third position with flat shipment growth sequentially at 4.0m units in Q2 2022. The newly launched Redmi 10 series coupled with its old Redmi 9 series led to robust sequential growth in four of the five largest SEA markets. The launch of Xiaomi’s POCO F4 series created a positive buzz for its online-centric sub-brand, driving shipments across its online channels.

vivo and realme complete the top five, shipping 3.2 million and 2.6 million units respectively. vivo launched a myriad of new devices such as its T1 series and Y01 series in certain strategic markets in Southeast Asia to give it access to a wider range of target groups across different price bands. While realme refreshed its flagship GT series in Q2 as it looks to reignite its efforts to improve branding.

The mid-high-end pricing range was hit hardest as customers cut back on consumer technology purchases due to increased costs for leisure and everyday requirements as Southeast Asia markets open up. However, Apple continued to be resilient in the face of economic uncertainty and the limited consequences of rising inflation on its affluent customer base. And with the timely launch of its SE series and the popularity of its iPhone 13 series, Apple maintained dominance in the premium price segment.

Market outlook

“The demand for 5G devices has come to a standstill,” said Canalys Research Analyst Chiew Le Xuan. “5G devices experienced their first sequential decline to 18% of overall smartphone shipments. 5G deployment in developing Southeast Asian markets has been abysmal ensuring the hype for 5G has dwindled, and demand has shifted to more practical aspects of smartphones such as battery life, storage, processor speed, and camera quality. Growing inflation has resulted in consumers looking for longer-lasting devices over less practical qualities such as 5G. Practical uses of 5G have yet to be seen, and is especially unnecessary for low-mid devices when 4G speeds are sufficient in day-to-day usage.

“Maintaining device affordability while boosting profitability is the greatest challenge for vendors. Competition in the entry-level segment has intensified with the introduction of many new products by android smartphone vendors. It is vital for vendors to optimize product portfolios to improve their branding and outreach. At the same time, vendors should be mindful of product cannibalization within the same price segment. However, the remainder of 2022 will be challenging for smartphone vendors as they have to tackle rising costs, forex volatility, and shrinking consumer demand. Vendors will have to keep a close eye on margins while competing aggressively to capture market share in price-sensitive Southeast Asia.”

|

Southeast Asia smartphone shipments and annual growth |

|||||

|

Vendor |

Q2 2022 |

Q2 2022 |

Q2 2021 |

Q2 2021 |

Annual |

|

Samsung |

5.7 |

23% |

5.4 |

20% |

4% |

|

OPPO |

4.4 |

18% |

4.9 |

18% |

-10% |

|

Xiaomi |

4.0 |

16% |

6.0 |

22% |

-34% |

|

vivo |

3.2 |

12% |

3.9 |

14% |

-18% |

|

realme |

2.6 |

11% |

3.3 |

12% |

-22% |

|

Others |

4.7 |

19% |

4.1 |

15% |

14% |

|

Total |

24.5 |

100% |

27.7 |

100% |

-11% |

|

|

|

|

|||

|

Note: Xiaomi estimates include sub-brand POCO and OPPO includes OnePlus. Percentages may not add up to 100% due to rounding. |

|

||||

For more information, please contact:

Chiew Le Xuan: lexuan_chiew@canalys.com +65 9655 6264

About Smartphone Analysis

Canalys’ worldwide Smartphone Analysis service provides a comprehensive country-level view of shipment estimates far in advance of our competitors. We provide quarterly market share data, timely historical data tracking, detailed analysis of storage, processors, memory, cameras and many other specs. We combine detailed worldwide statistics for all categories with Canalys’ unique data on shipments via tier-one and tier-two channels. The service also provides a unique view of end-user types. At the same time, we deliver regular analysis to give insights into the data, including the assumptions behind our forecast outlooks.

About Canalys

Canalys is an independent analyst company that strives to guide clients on the future of the technology industry and to think beyond the business models of the past. We deliver smart market insights to IT, channel and service provider professionals around the world. We stake our reputation on the quality of our data, our innovative use of technology and our high level of customer service.

Receiving updates

To receive media alerts directly, or for more information about our events, services or custom research and consulting capabilities, please contact us. Alternatively, you can email press@canalys.com.

Please click here to unsubscribe

Copyright © Canalys. All rights reserved.

For more information:

e-mail press@canalys.com

PDF download

Southeast Asian smartphone shipments fall 7% sequentially in Q2 2022

Southeast Asian smartphone shipments fall 7% sequentially in Q2 2022